2020 was the best year for e-commerce marketplaces in over a decade. E-commerce growth had a step change, and marketplaces captured most of it. In aggregate, it was the most successful year for sellers and brands that transact through them, too. The Year in Review looks at the state of marketplaces and describes the most important trends.

The press often focuses on the narratives that depict the Amazon marketplace as a hostile, unreliable, and unpredictable platform. Amazon should address all of them. But, while all true, those stores ignore the many businesses that manage to build and scale on it and many surrounding software and services firms that enable them. And more recently, investors who are funding and acquiring those businesses. Without dismissing the negatives, it is vital to notice the growth of sellers, the number of brands launched, and ultimately the growth of GMV.

Amazon marketplace added eBay’s worth of sales to its GMV this year. In 2020, sellers on the Amazon marketplace sold an estimated $295 billion worth of products, increasing their sales by $95 billion, up from $200 billion in 2019. Attracted by that, nearly $1 billion in fresh capital was committed to firms looking to acquire Amazon sellers and brands.

The Amazon seller is now in its third form. The Amazon seller 1.0 was a reseller. Advertising on Amazon and private label brands created the Amazon seller 2.0. The current seller - the Amazon seller 3.0 - is building Amazon-native brands, intentionally selling multi-channel, driving traffic from outside of Amazon, and investing in social commerce. The underlying Amazon marketplace building blocks remain the same, but the seller had to evolve to create more value and differentiate from the competition.

As e-commerce boomed during the pandemic, some marketplaces have greatly benefited, a few prepared for the future, while others were caught unprepared to react. Etsy, Walmart, Amazon, and to some degree, Target were the four winners. They each grew sales for different reasons, added more sellers, and strengthened their market share. Etsy grew the supply as demand increased the most impressively. Target grew the fastest, but its small invite-only seller base makes it hard to compare against much larger marketplaces.

Amazon didn’t increase its market share this year - it grew slower than most retailers and marketplaces, in part because it is bigger than most and because its fulfillment struggles early in the year sent shoppers to its rivals. This year has highlighted the vulnerability that stems from Amazon’s fulfillment operations: Amazon warehouses and ships practically everything sold on Amazon.

Google Shopping, Wish, and eBay were the three losers. eBay had two consecutive quarters of growth but is unlikely to retain the momentum. Wish had slow shipping times because it relies on China-based sellers, and its sales growth in the third-quarter was lagging. Google Shopping didn’t make any notable moves in trying to become an e-commerce channel - it remained a bystander powering top-of-the-funnel ads.

This report focuses on those seven marketplaces. There are hundreds more, especially internationally, and thousands of topics that weren’t included. Thus, this is a selective collection of insights and data. Unless otherwise noted, all data discussed is Marketplace Pulse data, while the financial data comes from companies’ quarterly earnings. There are inherent limitations to estimating most of the behavior on marketplaces; thus, it is often the direction of changes that is more telling than the point-in-time value.

Contents

Amazon Gross Merchandise Volume (GMV)

In 2020, sellers on the Amazon marketplace sold $295 billion worth of products, and as a retailer, Amazon’s sales were $180 billion. For a total Amazon gross merchandise volume of $475 billion, according to early and rough estimates based on Amazon disclosures.

Third-party sellers increased their sales by $95 billion in a year, up from $200 billion in 2019. Amazon’s sales grew by $45 billion, from $135 billion. Gross merchandise volume (GMV), the total amount of sales on Amazon websites, including those by the company itself and by the marketplace, grew from $335 in 2019 to $475 billion in 2020. GMV was up 42%, while first-party sales were up 35%, and third-party volume was up 47%. 62% of Amazon’s worldwide GMV was by the marketplace. Up from 60% in 2019 and 58% in 2018.

For the first time, in the second quarter, Amazon’s fastest-growing business segment was the marketplace. Revenue from transaction and fulfillment fees was up by an all-time-high 53% in the quarter, indicating strong sales by the marketplace sellers. Results in the third quarter matched the growth rate.

“Third-party sales again grew faster this quarter than Amazon’s first-party sales,” confirmed Jeff Bezos, CEO of Amazon, when discussing second-quarter results. The second quarter’s sales surge has elevated both the marketplace and first-party sales above Amazon’s previously fastest growing business segment - advertising.

“We buy and grow Amazon businesses”

Nearly $1 billion in fresh capital was committed in 2020 to firms looking to acquire Amazon sellers and brands (money invested is a mix of equity and debt). The market had a breakout year because of three factors: the pandemic accelerating spending on Amazon, Thrasio raising hundreds of millions of dollars, and Anker, an Amazon-native brand, going public.

- November 2020. SellerX Raises $118M to Buy Up and Grow Amazon Marketplace Businesses

- November 2020. Heyday Raises $175 Million to Buy Amazon Businesses

- November 2020. Razor Raises €25 Million to Acquire and Scale Amazon Brands

- November 2020. Heroes Raises $65M in Equity and Debt to Become the Thrasio of Europe

- October 2020. Perch Raises $123.5M to Grow Its Stable of D2C Brands That Sell on Amazon

- September 2020. Boosted Commerce: $87 Million Funding and Acquisition of Six Amazon Fulfillment Companie

- August 2020. Razor Raises €4 Million Seed Round

- July 2020. Thrasio Raises $260M, Reaches Unicorn Status With $1B Valuation

- April 2020. Thrasio Raises $100 Million in Fresh Capital

- April 2020. Perch Raises $8M to Acquire Top Performing ‘Fulfillment by Amazon’ Products and Companies

Accel Club, Acquco, Alpha Rock Capital, Boosted Commerce, Cap Hill Brands, Centro Brands, Dragonfly, Flywheel Commerce, GOJA, Heyday, Inflection Brands, Perch, Recombrands, Suma Brands, and Thrasio operate in the U.S. Brands United, Razor Group, Thirstii, SellerX, Zeelos, and Orange Brands operate in Germany. The United Kingdom has Heroes.

The capital pouring in is validating the Amazon marketplace as something serious. The businesses that sell on Amazon have grown mainly relying on measurable demand, controllable unit economics, and the predictability the data-rich marketplace provides through tools like Jungle Scout, Helium 10, and others. The firms rolling up those businesses use the same principles to evaluate and value them and grow them post-purchase. The types of companies those firms are looking to acquire are most often private-label sellers that use Amazon as one of their primary sources of distribution (some are also looking at brands using Shopify). There is no demand for resellers, nor do other marketplaces play a significant role.

Amazon-dependency is both the most significant risk and the fuel that powers those firms. But there are dozens of additional challenges yet to be resolved. For example: transferring the scrappiness of a one-person seller to an employee of a firm, long-term risk of brands on Amazon, building a brand vs. being operationally efficient, buying brands vs. building brands in-house, avoiding suspensions, and others. Money for most of those firms came first; they will spend the next year figuring out the model that could work and scale.

Today many of the firms are look-alike, using the same “we buy Amazon businesses, we close quickly, we have a smooth process” messaging. As more capital continues to flow in, there will be more focus spent on differentiating. “We buy Amazon businesses” is already an outdated concept. Some are already focusing on particular categories; some are investing in exchange for a minority stake. Others want to be incubators for more brands like Anker.

The largest firms modularize Amazon seller operations. Rather than an individual seller trying to be great at sourcing, importing, marketing, financial planning, and omnichannel, those firms run the portfolio by having each area handled by a team of experts. The best are building in-house technology to handle crucial tasks. Amazon’s search algorithms do not rank larger sellers higher, but small sellers (often under-capitalized and over-leveraged) are unlikely to out-run the best-operating firms.

Some firms are e-commerce teams with no investment experience. Some are seasoned investors with no e-commerce experience, let alone Amazon marketplace experience. They will hire for jobs outside of their areas of expertise and utilize agencies to take care of the rest. The operational complexity required to handle and grow dozens of hundreds of Amazon sellers is perhaps currently under-appreciated, thus as those firms scale, some will struggle. 101 Commerce from Austin, Texas, was one of the first firms to enter this market in 2017. It had the right talent, experience, and capital. But it appears to have failed and has since been integrated into GOJA. A few other less-known firms in this space have also shut down or pivoted to building brands rather than acquiring them.

Likely the acquisition multiples will increase. As more firms compete for the same businesses, some will be able to negotiate a higher price. Maybe prices will rise overall. If they do, that will invite even more entrepreneurs to pursue selling on Amazon since the exit plan is simple and predictable.

A few years from now, some of those firms will be worth much more than the parts purchased at 2.5-4x (they acquire businesses at 2.5-4x EBIDTA multiple with earn-out). Performing a roll-up strategy in a fragmented but growing market is a common strategy in private equity.

COVID Impact

Demand for essentials like toilet paper, hand sanitizers, paper towels, n95 face masks, and thermometers reached a peak in March. By the end of the year, considerably fewer shoppers were looking for those products. In March, 46 out of the top 100 most-searched keywords on Amazon were essentials related. The figure decreased to just 3 in December.

To limit overall sales on Amazon, in March, the company removed the deals page and product recommendations from the homepage, eliminated the frequently bought together list, and didn’t accept new discount coupons from brands. Brian Olsavsky, Chief Financial Officer of Amazon, said, “we cut marketing probably by about a third in Q2, mainly because we’re trying to manage demand.” It implemented those changes to achieve something it never did before - to reduce shopping on Amazon.

The company was trying to focus its operations and, thus, consumer spending too, on essentials and high-demand items. “We typically want to sell as much as we can, but our entire network is so full right now with just hand sanitizers and toilet paper that we don’t have the capacity to serve other demand,” said an Amazon employee involved in the changes, quoted by The Wall Street Journal.

Amazon experienced all-time high negative seller reviews in May. Seller reviews are the best indicator of Amazon shopper sentiment since they capture as many as ten million opinions a month. In 85 days between February 29th and May 24th, the share of positive reviews on Amazon worldwide marketplaces dropped from 92.5% to 88.7%. It then took nearly as long - until August 12th - to recover.

In May, Amazon shoppers left an all-time high of one million negative seller reviews. Nearly three times more than in March, and almost double the previous record. Failed delivery promises were the most common cause. 49% of reviews mentioned keywords like “never,” “received,” “tracking,” “package,” “late,” or “delivery.”

Increased negative experiences shoppers had were caused in part by Amazon’s fulfillment struggles that caused sellers to sell out of inventory stored in Fulfillment by Amazon (FBA) and thus reduced Prime-enabled assortment. The timeline when negative reviews skyrocketed matches the drop in Prime-enabled sellers. From late February to early August, more marketplace sales were fulfilled by merchants than usual.

Small vs. Big Sellers

As the overall Amazon marketplace GMV expands, top sellers represent a shrinking percent. More of the sales come from a broader set of sellers than the top sellers outpacing the rest. The data indicates that it is getting harder for large sellers to continue growing because it is getting easier for new sellers to start selling.

Just 850 sellers were responsible for 10% of Amazon’s worldwide volume. But more than 38,000 sellers were responsible for 50%. Finally, more than 360,000 sellers were responsible for 90% of the volume. The size of each percentage bucket has not remained consistent over the years, however. The number of sellers it takes to contribute 10% is growing faster than the number of sellers contributing 50%. It takes more of the top sellers to result in 10% of volume.

The majority of sales volume on the Amazon marketplace comes from sellers that have been on it for years. That signals the controlled churn and high longevity of those businesses. At the same time, new sellers bring incremental growth - they are not necessarily replacing past ones. In other words, the marketplace is not saturated because new sellers are finding opportunities to grow. Thus by reason, they are not the same as existing sellers and are selling in different niches.

In the four biggest markets - the U.S., the U.K., Germany, and Japan - more than half of the volume are by sellers who joined in 2017 or earlier.

Active sellers typically remain so for multiple years. For example, 84% of the top 10,000 sellers in 2015 continued to be active sellers through their third year on Amazon. 89% of top sellers continued to be active two years later, and 95% continued to be active after one year. These percentages hold for the top sellers from 2015, 2016, 2017, 2018, and 2019.

Private-Label Sellers

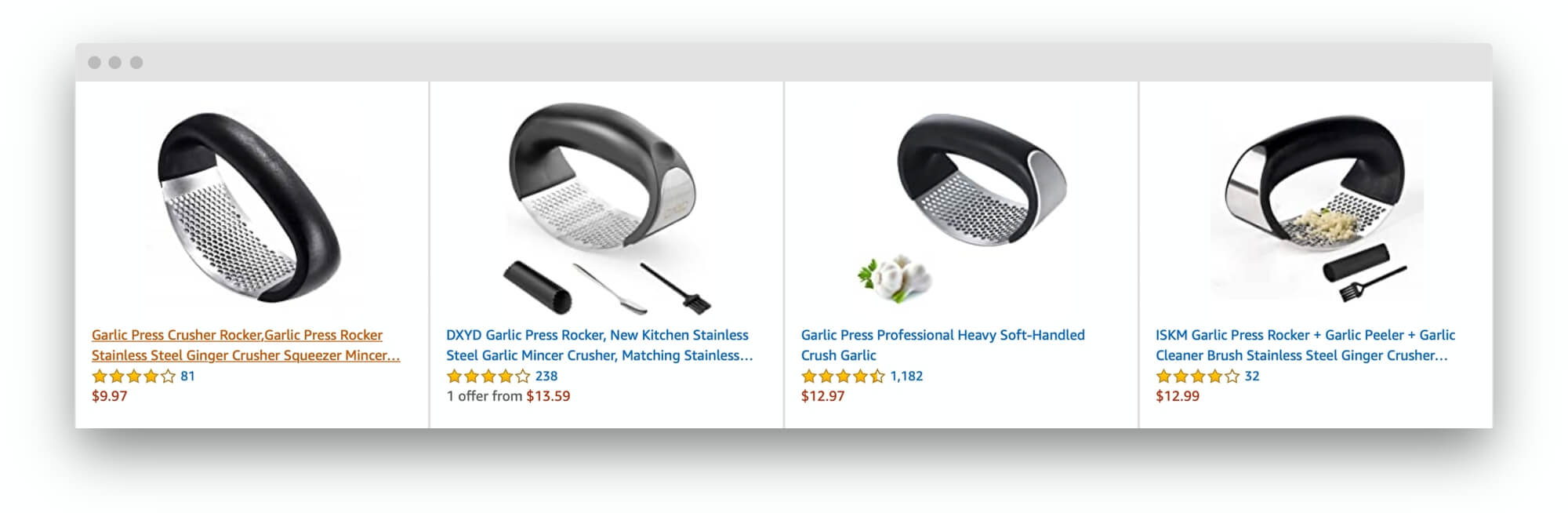

A garlic press is a product made infamous by private-label selling courses. Many sellers continue to launch their versions - 1,760 different products were in the top 100 best-selling garlic presses since January 2019. That’s more than two new products from often two new brands every day replacing previous items in the top 100 list. Most of them look nearly identical, but all of them try to stand out. And because the best-sellers are unrecognizable brands, that enables launching new, also unrecognizable brands.

Less than half of the 1,760 products were in the top 100 for more than ten days, and just 20% were in it for more than fifty days. The instability of high-demand categories is a testament to how easily sellers can launch a temporarily best-selling product. Even if those products end up falling off the next day - sometimes because Amazon suspended the listing after finding reviews manipulation, for example - it gets replaced by more of the same. After all, creating a new brand on Amazon has zero marginal cost.

Most categories do not have a brand that owns them, in the sense of shoppers explicitly looking for a specific brand when searching for a product. Shoppers search for “garlic press,” “garlic mincer,” “garlic chopper,” and “garlic press stainless steel,” rather than, for example, the OXO garlic press, a product that is one of the best-sellers. Those types of searches - most searches on Amazon - are the perfect breeding ground for private label products. The products that Amazon selects as the first organic results plus those that bought ads get bought, unmindful of the brand.

Two products have been in the top 100 for the full two years. Almost forty have been in it for over 500 days (70% of the time). Thus while the instability means many products are trying to get into the top 100 and often succeeding, some products manage to stay best-sellers despite the competition. Those products are trying to become Amazon-native brands, launched on and for Amazon; similar to Digitally native vertical brands (DNVBs), which are born on the internet, Amazon-native brands are leveraging Amazon.

Sellers Growth

The number of sellers on Amazon didn’t accelerate, despite the sales boom during the pandemic. This mismatch between supply and demand is a gap that existing sellers are filling.

Amazon added more than 1.3 million new sellers in 2020. Since the start of 2017, more than 4.5 million new sellers have joined. It continues to add 3,500 new sellers every day, or 146 every hour, or even two every minute. Yet those numbers look identical to the past three years.

Over 190,000 new sellers joined the Amazon marketplace in the U.S. over the past twelve months; nearly 75,000 of those sellers were U.S.-based. Businesses from California, Florida, Texas, New York, and New Jersey represented almost half of them. California based sellers represented 17.5% of the new sellers. Florida had 12.1%, Texas 8.2%, New York 7.7%, and New Jersey 4.1%. The rest of the states combine to 50.4%. Adjusted for per capita, Wyoming and Delaware top the list instead.

The top 10 cities with the most sellers were Miami, Brooklyn, Los Angeles, Houston, New York, Las Vegas, Orlando, San Diego, Chicago, and Dallas. Miami is home to the “South Florida FBA - Amazon Sellers,” the country’s largest regular community group with over 4,200 members on Meetup.com.

Amazon has attracted 700,000 sellers - mostly local micro-enterprises - to join its India marketplace since it launched in the country in 2013. By the end of 2020, India surpassed the U.K. and Germany marketplaces to became the second largest marketplace in terms of the number of sellers. However, only 5,000 sellers had sales worth at least $13,570 (INR 1MM) during the Great Indian Festival on October 16th-18th, 2020. But, 110,000 sellers had at least one order. Thus, Amazon India exhibits the Marketplaces Power Law (perhaps even more extreme than other marketplaces).

On a trip to India early in 2020, Jeff Bezos, CEO at Amazon, talked about its plans to bring more than 10 million micro, small, and medium-sized businesses online by 2025. The critical term is micro because Amazon is looking to onboard a different set of sellers than in other key markets - it doesn’t need 10 million sellers in the U.S. or Europe. Despite adding more than 100,000 new sellers every year since 2016 and continuing to accelerate, the growth rate will have to rise drastically, though, to achieve 10 million by 2025. To enable those micro-sellers, Amazon had to do India-first innovations. Like allowing registering and managing the seller account only using a smartphone.

“Every other locale we operated in until we came to India, we didn’t have to worry about seller awareness or whether they were used to a laptop or not. But, India is unique. Many sellers hadn’t even seen a laptop until then, and the fact that they didn’t even want to leverage the technology opportunity was new for us,” said Gopal Pillai, Director and General Manager of Seller Services, Amazon India, in 2018.

China Sellers

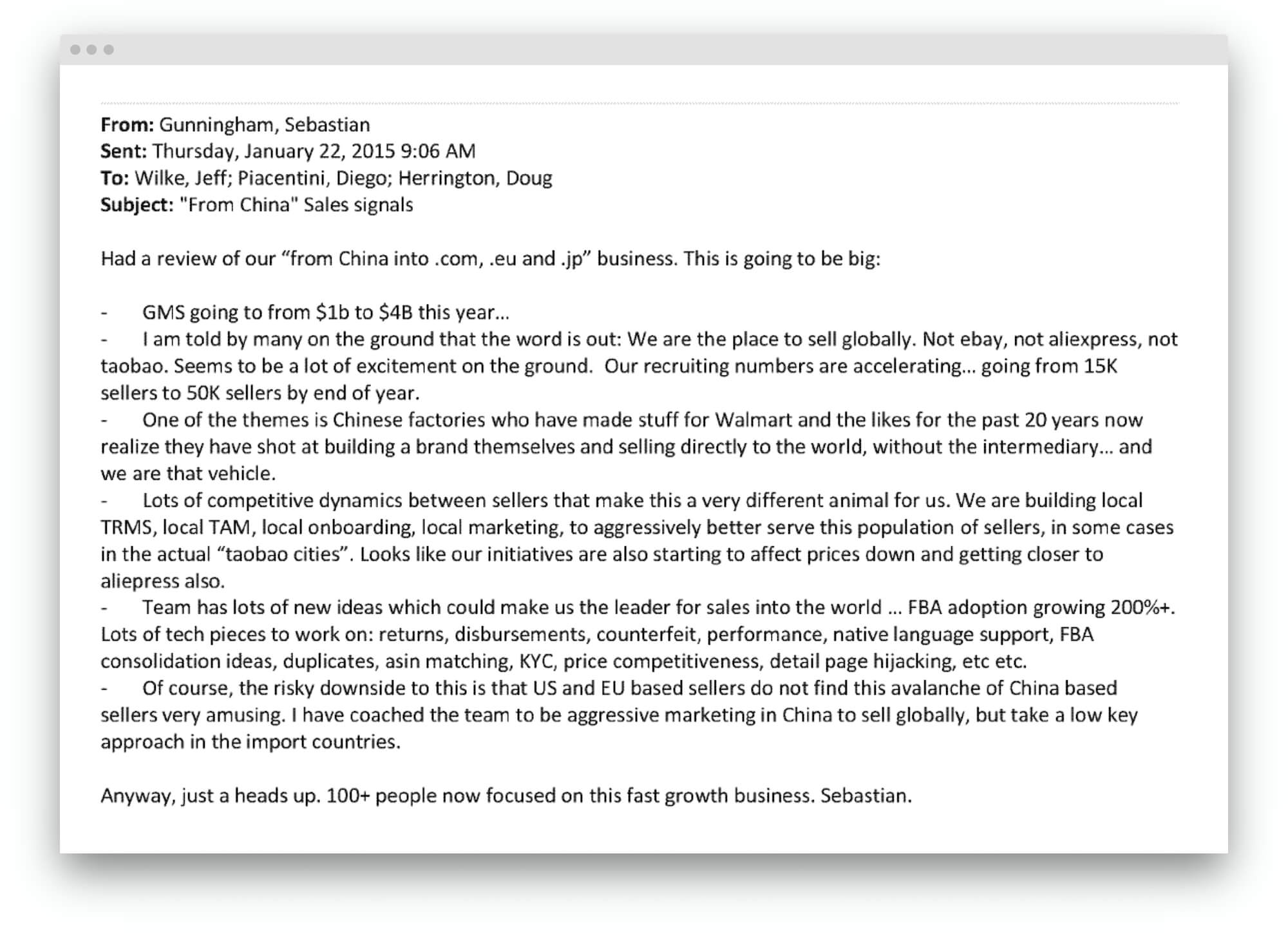

“One of the themes is Chinese factories who made stuff for Walmart and the likes for the past 20 years now realize they have shot at building a brand themselves and selling directly to the world, without the intermediary… and we are that vehicle.” Wrote Sebastian Gunningham, senior vice president of Amazon Marketplace at the time, in an internal email from 2015 released by the House Judiciary Committee in 2020. Sebastian Gunningham started the email with, “this is going to be big.” According to the email, China-based GMV was just $1 billion in 2014.

“Let’s cut out the middleman,” said Geoffrey Stewart, an Amazon employee in Shenzhen, at a 2019 April trade event in Hong Kong in a video the Wall Street Journal viewed. “We think that will enhance margins for our manufacturing partners, and it will delight customers.” Amazon wasn’t the only platform that allowed that, but its Fulfillment by Amazon (FBA) created a shopping experience that eliminated long delivery times often associated with buying from China.

Share of top Amazon sellers by China-based businesses shrank starting February until May because of disruption to manufacturing, freight, and warehousing, as well as consumers prioritizing essentials. 30% of the top sellers in the four core Amazon markets - U.S., U.K., Germany, and Japan - were based in China in May. Down from 36% in January. The percent is the average of the four marketplaces.

Four years ago, in May 2016, only 11% of the top sellers were based in China. Since then, the share has continued to grow steadily. The same behavior is true for the North American marketplaces in the U.S., Canada, Mexico, and European marketplaces in the U.K., Germany, France, Italy, Spain, and Japan. All marketplaces started to reverse the trend beginning in February.

Nonetheless, by the end of 2020, the share of top Amazon sellers from China reached an all-time high of 42%.

Most of Amazon’s marketplace sales volume on its worldwide marketplaces comes from first, domestic, and second, Chinese sellers. Other countries combined represent a small percentage. In countries like France, Italy, Spain, Mexico, and Canada, China even represents a larger share than the domestic sellers. No international market, except for China, represents more than 1% of sales in the U.S. marketplace, even though nine more countries - Canada, U.K., India, Japan, Australia, Vietnam, Thailand, South Korea, and Ukraine - have more than 10,000 sellers.

Sales volume share is modeled using the total feedback reviews grouped by the seller’s business country. For example, more than 500,000 sellers on Amazon.com received a feedback review over the last twelve months totaling over 51 million reviews. 52% of those reviews were for sellers based in the U.S., 42% were for sellers based in China.

The critical finding is not the exact percentages, but rather that cross-border selling on Amazon is concentrated in a few countries. For example, there is little overlap between Europe and the U.S.: European sellers represent a small percentage of the U.S. volume, and few U.S. sellers are booming in Europe.

Since March, more than half of the new sellers on Amazon in the U.S. were from China. In March, growth resumes. 50% of sellers in March were from China, an increase from 36% in 2019. Every year, February sees the smallest number of new Chinese sellers due to the Chinese New Year, virtually shutting down the country for two weeks.

Fulfillment by Amazon (FBA)

The Prime-enabled assortment suffered after Amazon’s decision in March to temporarily stop accepting shipments of non-essential goods to its warehouses that resulted in supply disruption. From May to July, a twelve month low of the top Amazon sellers offered Prime shipping for most of their catalog. However, by September, the Prime assortment had recovered.

This year has highlighted the vulnerability that stems from Amazon’s fulfillment operations: Amazon warehouses and ships practically everything sold on Amazon. That includes products sold by the company and its vast marketplace because most of the third-party sellers rely on Fulfillment by Amazon (FBA). The same FBA moat that allows the company to provide a consistent shopping experience despite millions of sellers behind the scenes is a single point of failure.

The elasticity of Fulfillment by Amazon (FBA) broke first in March when the company prioritized stocking household staples and medical supplies. To do so, it disabled inbound shipments to FBA for products that do not fall into the essentials or high-demand categories. Because no new inventory was allowed into Amazon warehouses, it caused stock-outs as items continued to sell. A few months later, all items were allowed to be shipped to FBA again, but some shipments took weeks to get received. “Inventory was shipped to FTW1 (aka Dallas) and typically takes maybe 1 to 2 days for delivery and about 2 days for checkin. Now it’s been over 3 weeks,” one seller said.

Then, in July, the company imposed quantity restrictions for new products and limited others based on recent sales history. “Even though it’s July, we’re preparing early for the holiday season to meet sustained increased demand,” the company wrote to sellers in an email. By the end of November, to relieve some pressure from the FBA network, the company started diverting some sales volume to sellers fulfilling orders themselves. And quantity limits got even more restrictive. As product demand increased in the fourth quarter, the FBA quantity limit instead decreased.

“I am noticing my limits getting smaller and smaller every week. My stock limits are under 30 days for some items that sell over 40 units a day, and check-in takes 50 days,” one seller said. “We’re the #1 seller in our category and have a low stock alert but can only ship in ~ 500 more units today due to inventory limits,” added another. “I sell around 1060 a month of this product. A few weeks ago, I was allowed to send in 2000, now my maximum is 1300,” and “Wow, an SKU with 2000 allowed just got cut down to <600” added two more sellers.

None of this is surprising given the rate of e-commerce growth and fulfillment constraints that came with it. “We’ve run out of space,” said Brian Olsavsky, Chief Financial Officer at Amazon, during the company’s second-quarter earnings call. He added that the company increased the fulfillment network square footage by 15% in 2019 and expects a 50% increase in 2020. Amazon also added 427,300 employees between January and October, growing its workforce to more than 1.2 million people globally, according to Karen Weise of the New York Times. Despite the enormity of these figures, that appears to have not been enough.

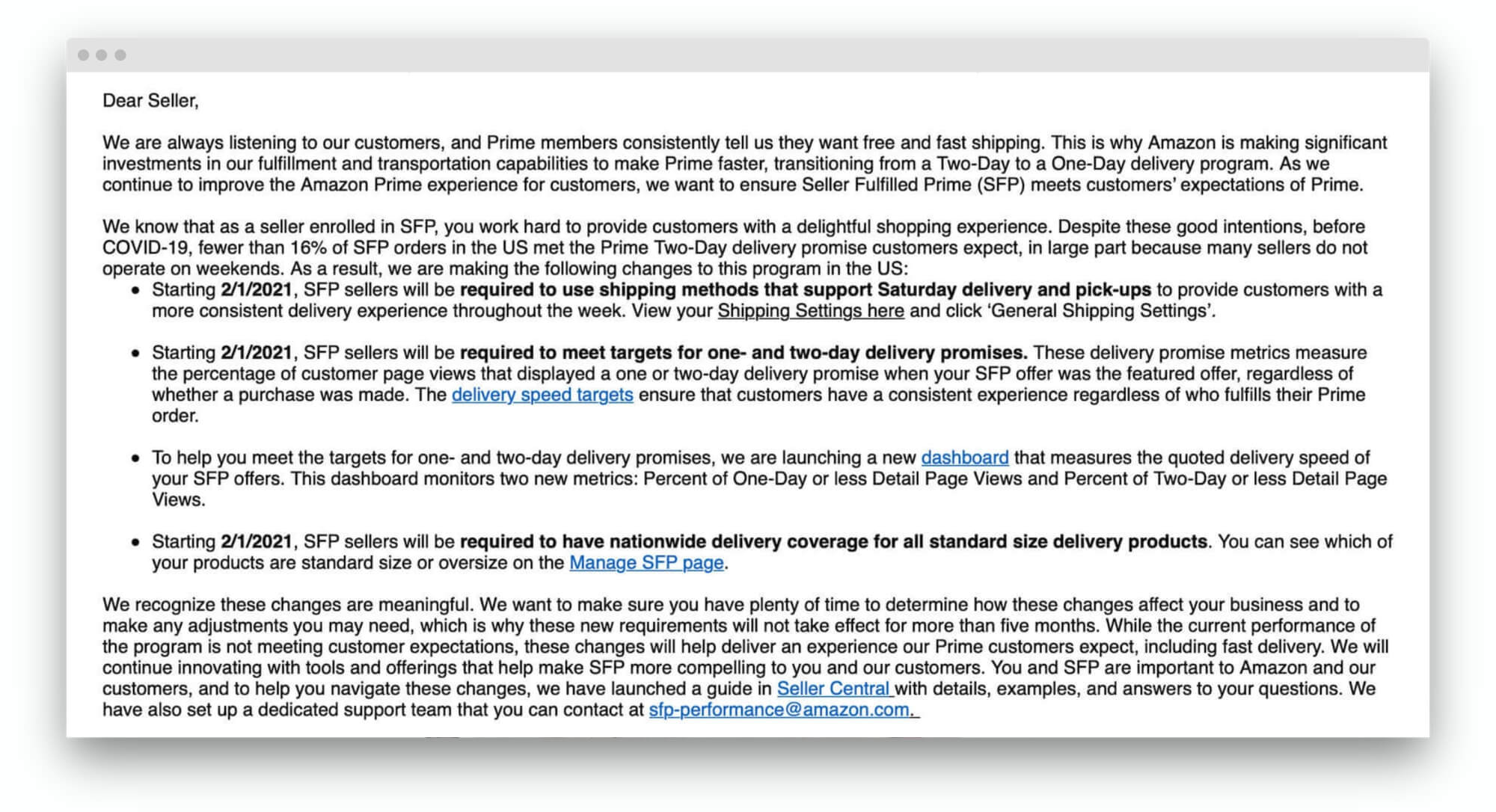

In August, the Seller Fulfilled Prime (SFP) program that enables marketplace sellers to offer Prime shipping without using Amazon’s warehouses had several changes announced that increased performance requirements fewer sellers will be able to meet. While the SFP program is technically still operational, it is now limited to only the biggest sellers.

In theory, SFP allows sellers to sell products with the Prime badge directly from their warehouse and enables Amazon to increase Prime assortment without building ever-more warehouse space. In practice, few sellers were allowed to join the SFP program before it closed for new registrations in early 2019, and the ones that did often didn’t meet the performance standards Amazon expected. “Fewer than 16% of SFP orders in the U.S. met the Prime Two-Day delivery promise,” the company said in a note to sellers.

Starting February 2021, Amazon will require sellers to use shipping methods that support Saturday delivery and pick-ups, have nationwide delivery coverage for all standard size delivery products, and meet targets for one and two-day delivery promises. The changes introduced will improve the overall on-time delivery metric. However, they will achieve that by reducing the number of sellers participating in the program and the number of products offered.

Amazon’s goal is nationwide one-day delivery. Only a small number - less than ten - of sellers can offer that, however. Amazon’s secondary objective is consistent availability across the country on all days of the week. Sellers can offer two-day and one-day Prime delivery in some parts of the country and sometimes only on workdays. That’s what the SFP program previously allowed them to do. But new requirements mean only the biggest sellers with warehouses operating on weekends will be able to meet them. Some third-party logistics companies could meet them too, but Amazon doesn’t appear to be interested in enabling that.

Anker Goes Public

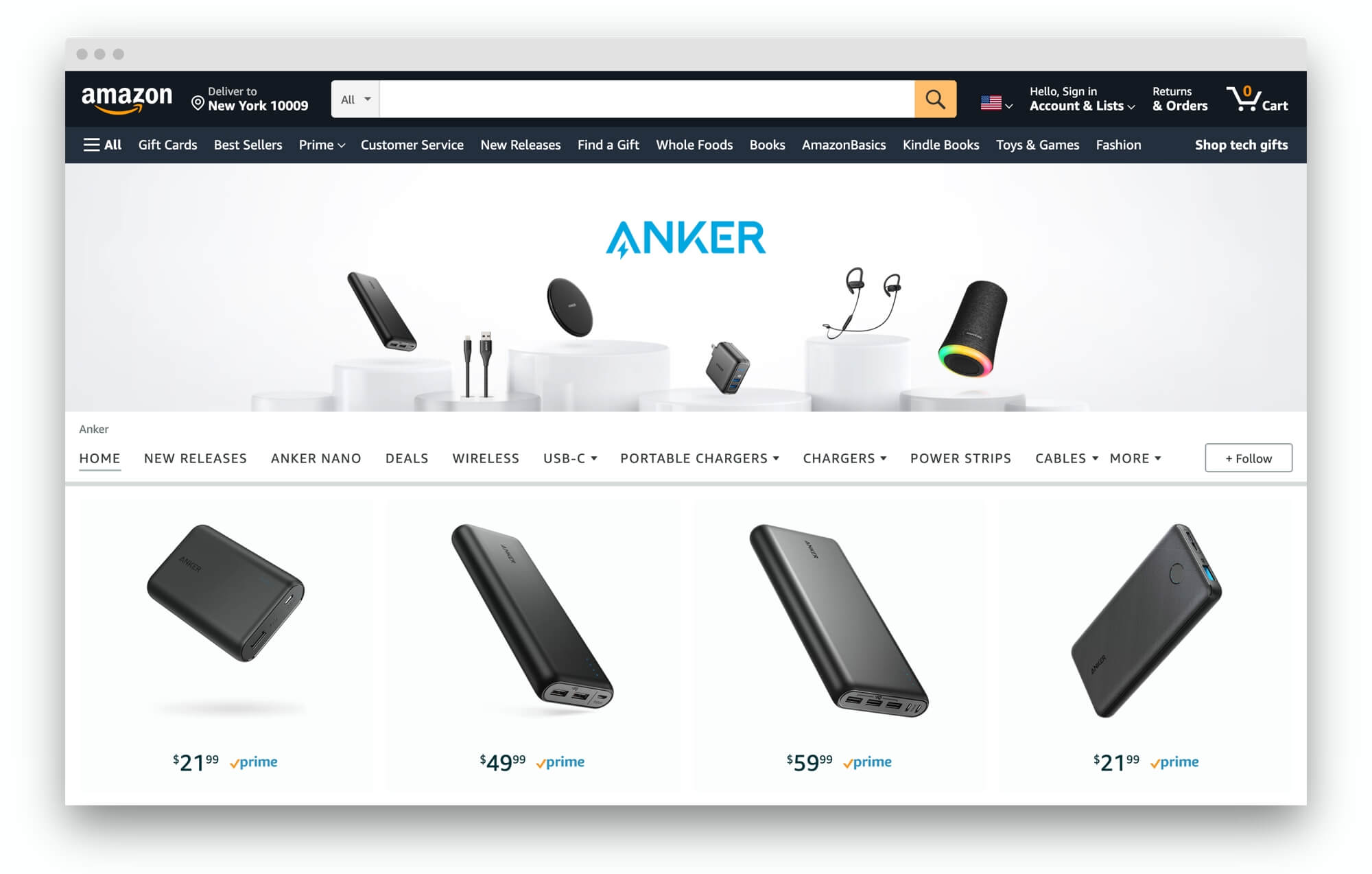

Anker, a Chinese brand founded in 2011 by ex-Google engineer Steven Yang, debuted on the Shenzhen Stock Exchange on August 24th. The brand was one of the first Amazon-native brands. It surpassed $1 billion in sales in 2020. The company had a market cap of over $8 billion at the end of the first trading day. It had an $11 billion market cap by the end of 2020.

Anker launched before most Chinese companies realized Amazon could be a channel to sell directly to the U.S. and other markets. In 2011, it was years before Amazon itself would recognize it. Anker has since expanded to other marketplaces and established vendor relationships with offline retailers like Best Buy, Walmart, and Apple. However, Amazon has remained a key channel. Anker sells directly as a third-party marketplace seller on Amazon worldwide marketplaces. It is one of the biggest sellers on all of them.

2011 was also before most domestic brands realized the importance of Amazon. That gave Anker a multi-year headstart to grow on Amazon and start building brand recognition. By the time other Chinese and local brands noticed this, Anker was well ahead. The brand utilized this position to innovate on technology (the company claims that 50% of staff work in R&D and it has more than a thousand patents) and launch new brands like Soundcore, Nebula, ROAV, eufy.

Anker has since attracted hordes of competition but hasn’t given up its position among best-sellers. 90% of the time over the past two years, Anker’s power bank was the number one best-seller in its category; the lowest it dipped was #5. It has amassed tens of thousands of customer reviews and retains a 4.8 out of 5 stars rating.

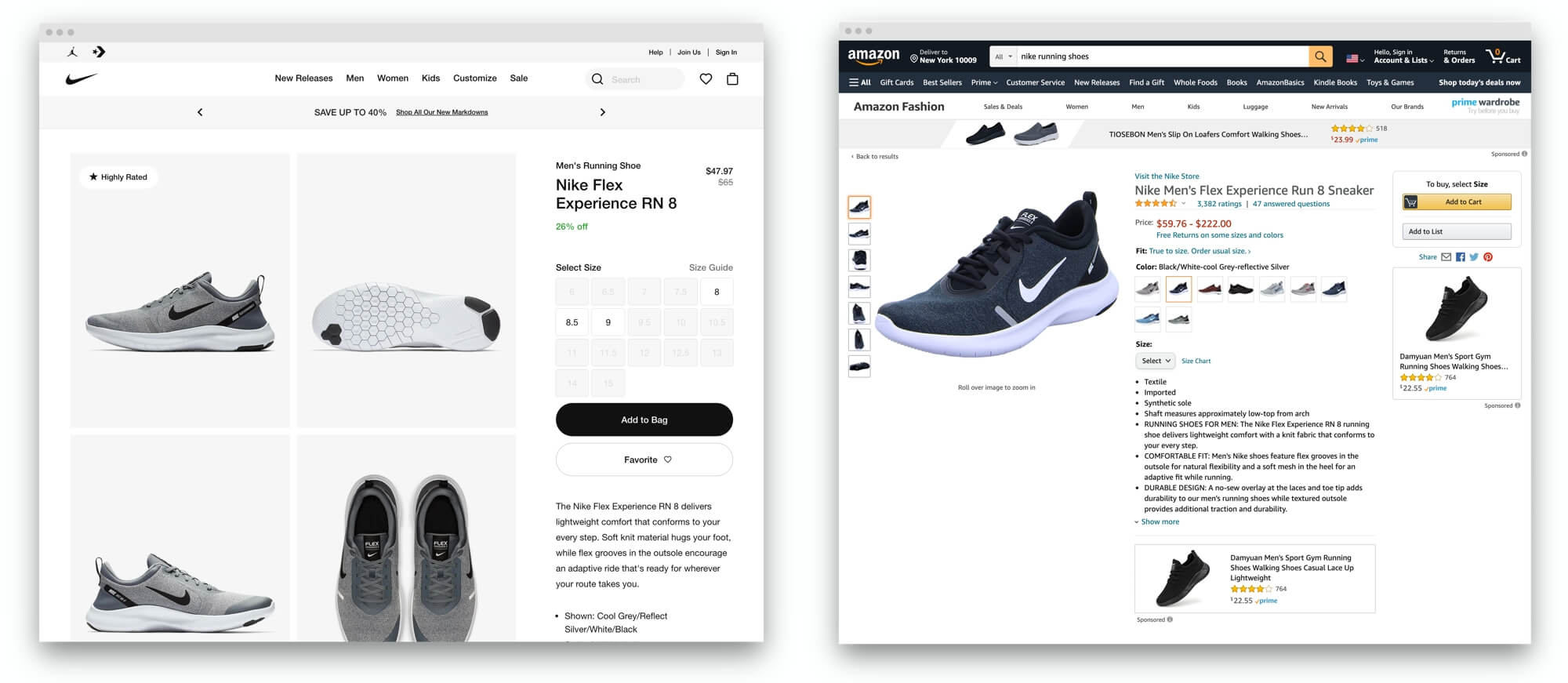

Nike Doesn’t Need Amazon

In November 2019, Nike stopped selling its goods wholesale to Amazon. It didn’t need Amazon at the time, and it needs them even less today - accelerated by the COVID-19 outbreak, direct e-commerce jumped to 30% of Nike’s sales, a mark it had previously expected to hit only in 2023.

Amazon, on the other hand, does need Nike. After the split, the possible scenarios were that Amazon would find a different way to source Nike goods wholesale, the third-party marketplace would source the full catalog, or that Nike would reverse its decision. None happened. Shoppers instead bought other brands. For example, in the Men’s Running Shoes category, Nike was one of the best-sellers for years. Amazon sold out by the end of 2019, and since then, the best selling Nike product has been averaging #15 place.

“As part of Nike’s focus on elevating consumer experiences through more direct, personal relationships, we have made the decision to complete our current pilot with Amazon Retail,” said the company in November 2019. Nike only agreed to the pilot in 2017 in exchange for Amazon policing counterfeit and third-party sales. The pilot didn’t work, and thus the brand never brought its full catalog to Amazon. But shoppers didn’t stop looking for Nike on Amazon - searches for its products have remained in the top 1,000 most-searched terms. The third-party marketplace continues to provide some, though limited, selection. It has subpar product pages compared to category-leaders. Other brands are bidding on Nike-related keywords to appear as ads instead.

Nike is likely okay with being presented poorly on Amazon. That makes shoppers go to Nike.com or download its app instead. The strategy is working because Nike is averaging 100 million visits to its website and is one of the top 10 most-downloaded shopping apps. As a result, Nike’s online sales were up 83% in the second quarter, adding $900 million to its total sales.

Nike’s departure from Amazon sent waves through the brands’ ecosystem. However, Nike is an exception. Meaning, Nike looks for channels that can create new growth. For it, Amazon could sell - Nike would argue poorly - to its existing audience. That audience is increasingly taking the extra steps to transact directly with Nike. It doesn’t need to accept the tradeoffs of selling on Amazon at the expense of maximizing revenue. Nike realized that it doesn’t need to fix its issues with Amazon. It could instead build a channel without those issues. Nike is focusing on what it can control and ignoring what it can’t.

Significantly More Products Reviews

Popular products on Amazon have significantly increased the number of reviews and raised the overall star rating since the company introduced one-tap ratings in October 2019. The company expanded product reviews by allowing shoppers to leave a star rating without a written review. Since then, the overall star rating has been based on traditional written reviews, one-tap ratings, and global reviews from Amazon’s international marketplaces.

In many categories, the top sellers now have tens of thousands - or, sometimes, hundreds of thousands - of ratings. That means new entrants have to do more to compete against what appears universally-liked products. The number of reviews a product needs to have to stand out by the end of 2020 is drastically different from just a year before. Also, since products now more easily gain ratings, they drown out some of the fake reviews.

For example, Apple AirPods have a 4.8 out of 5 rating based on 245,000 global ratings. Only 23,000 of those ratings are traditional reviews; the rest - over 90% - are the one-tap ratings. For the second half of 2020, it was receiving over 1,000 new ratings a day. It reached 2,000 a few dozen times.

Apple AirPods are in the Headphones category on Amazon. The average number of reviews per product increased from over 4,000 in 2019 to nearly 25,000 in December 2020 for products in the top 100, while the average rating rose from 4.1 to 4.4 out of 5. Half of the top 100 are now products with at least 10,000 reviews, more than double the amount a year ago. Many other categories exhibit the same change.

Shoppers are more likely to leave no review and instead use the one-tap rating when they had a positive experience. That’s why Apple AirPods have 218,000 five-star ratings, of which only ten percent are traditional reviews. Compared to one-star ratings, where regular reviews represent nearly half of all ratings.

But, Apple AirPods have nearly 3,000 one-star ratings without a written review. They are worthless for future shoppers trying to decide what are the reasons some dislike them. Those ratings are also not useful feedback to brands that previously relied on reviews to inform future product changes. Additionally, ratings are less transparent than reviews since Amazon doesn’t show who and when left it (data points some people and external tools used to check for fake reviews).

Amazon has removed the friction of writing reviews - a one-tap rating takes significantly less time. Unsurprisingly, that has resulted in popular products amassing ratings more rapidly and led to higher overall star ratings. Amazon’s own Echo Dot now has over 832,000 ratings - it only had 68,000 a year ago. Most shoppers browsing Amazon see more choices they would trust, even if many are unfamiliar with the introduction of ratings.

Amazon Advertising

The average cost-per-click (CPC) on Amazon ads is $0.85, according to Quartile Digital data. Despite more brands flocking to advertise on Amazon and the net ad spend increasing (nearly $13 billion was spent on Amazon ads in the U.S. this year), Amazon has also increased the ad inventory on and off Amazon and introduced new ad types. Against common belief, the average CPC has not increased this year. Instead, as some brands sold out of inventory and thus competition for ads decreased, it even declined a little.

The average advertising cost of sale (ACoS) is 22%. ACoS is the total ad spend divided by the total sales. The average conversion rate, the percentage of clicks an ad converts into sales, is 12.5%. Thus the average cost of sale is $6-$7 - it takes eight clicks at the average cost of $0.85 to generate one sale. Typically, 62% of sales are organic for private label sellers.

Private label sellers were the first to utilize advertisement on Amazon to scale their businesses (it made little sense for reseller-type sellers), and they continue to adopt new Amazon ad technologies the fastest. National brands have the biggest budgets, but the most efficient ads are usually by private label sellers. National brands also bring a digital marketing approach from their other channels, which is less specialized and underperforms on Amazon. They also tend to rely on shoppers searching for the brand explicitly, while private label sellers learned that most searches on Amazon are unbranded and tuned their strategies for that. That allows many private label sellers to outsell national brands on Amazon.

Amazon is spending on marketing to increase the number of shoppers, which attracts brands to buy more advertising, recouping most of Amazon’s marketing expenses. An advertising arbitrage flywheel. The company spent $5.4 billion on marketing-related expenses in the third quarter of 2020 but captured $5.3 in revenues from hosting advertising. That’s 99% of marketing expenses covered by advertising revenue. For comparison, Facebook’s advertising revenue represented 626% of marketing expenses, and Google’s was 544%. Both spend considerably less on marketing than Amazon but generate more revenue from hosting advertising.

The share of marketing expenses compared to advertising revenue has been on an accelerated rise since 2015. In 2015, advertising revenue represented only 32% of marketing expenses. It grew to 41% in 2016, 46% in 2017, 73% in 2018, 75% in 2019, and 93% in 2020. Amazon reports advertising revenue as Other Sales. Marketing expenses include costs associated with various marketing channels, payroll, and related costs for the marketing personnel.

The Number of Products Is Infinite

Amazon’s sales growth is unrelated to its catalog increase. No matter how many products Amazon adds to the catalog, there are only 48 items on the first page of search results. The outdated retail concept of the catalog size disregards the nuances of e-commerce, where shelf space has no cost and is thus endless.

There is a cliché that Amazon has infinite shelf space. Technically it does, as it can support a virtually endless number of products since each has a zero marginal cost. However, most shoppers will only see a few options before making a purchase decision. Amazon has an infinite number of shelves, instead of one endless shelf. Each search keyword has one that is a couple of dozen products long.

It’s not the shelf’s depth that matters; it is how to get customers to find what they need. Whether Amazon had twenty-five million t-shirts last year and has now doubled to one hundred million, it does not inform if customers are buying more t-shirts. At some number, the scale breaks, and the metric becomes meaningless. On Amazon, it broke many years ago. Millions of marketplace sellers have brought hundreds of millions of products, creating an explosion in catalog size. Auto-generated merchandise that gets manufactured on demand, drop-shippers with access to millions of SKUs from major distributors, and endless private label experiments continue to add daily.

However, the paradox of an infinite shelf is that while few products generate significant sales, many contribute a few. As a result, total sales are higher than that of a curated and thus constricted shelf. “A very, very big number (the products in the tail) multiplied by a relatively small number (the sales of each) is still equal to a very, very big number,” wrote Chris Anderson in the book “The Long Tail.” Therefore an endless catalog is valuable because it is better than predicting a short selection of top-performer products. However, the hidden cost of an infinite catalog is the inability to manage it without automation. Issues of counterfeits, product safety, or even editorial decisions not to sell certain items are near-impossible challenges.

Product prices, fulfillment options, and brand selection on the supply side are table stakes. Ignoring minor differences, Amazon and its competition have many of the same products and shipped quickly at the same prices. The supply side is not where differentiation happens for large retailers. There are brands that Walmart doesn’t carry and items that are cheaper on eBay, but Walmart’s and eBay’s catalog size comparison to that of Amazon doesn’t answer that. A marketplace’s goal is to have broad enough selection that it appears endless; beyond that, it stops being a significant number.

What matters for horizontal marketplaces like Amazon is the demand side. Curation, recommendations, search quality, advertising, live video, and others. The high number of products on Amazon is one of its challenges, rather than principal strengths, as it attempts to surface the most relevant products out of an endless pool of seemingly similar options. That’s why advertising is growing in importance - without it, getting to the front of the shelf takes time, and new product launches risk never being discovered.

Amazon Private-Label Brands

AmazonBasics products did not benefit from the pandemic opportunity - the number of AmazonBasics best-sellers has remained flat for over twelve months. Generally, private label products do well in periods of recessions and pandemics. Amazon’s private-label products did not. A best-seller AmazonBasics product is defined as having made it into the top 10 best selling products in any category on Amazon. Some of the AmazonBasics products are widely popular, like batteries and various cables, but the brand includes many niche products that only compete in their particular subcategory.

Despite Amazon launching more products, experimenting with ways to feature them in search, reports of accessing third-party sellers’ data to develop them, the flat line of best-sellers indicates that those efforts have generally been unsuccessful. The number of best-sellers in the wider top 100 has also flattened by May after increasing for years; in April, it had doubled from two years ago. By the end of the summer, it has started to decline.

In response to House Antitrust Subcommittee questions following the July 29th hearing, Jeff Bezos included a breakdown by department of Amazon’s private-label brands share of total first-party sales. It revealed that 9% of its sales in the Clothing, Shoes & Accessories department are from its private-label brands. Amazon’s most successful clothing brands are Amazon Essentials (men’s and women’s clothing), Simple Joys by Carter’s (children’s clothing), Goodthreads (men’s clothing), Daily Ritual (women’s clothing), and Lark & Ro (women’s clothing). The Clothing department has the most brands launched by the company.

In the Home & Kitchen department, private label brands represented 4%, in Consumer Electronics, they represented 3%, and in Consumables, they represented 2% of the company’s first-party sales in 2019. In other departments, private label brands represented less than 1% of the company’s sales.

| Category | First-Party % of Total Sales $ | Private Brand % of First-Party | Third-Party % of Total Sales $ |

|---|---|---|---|

| Consumer Electronics | 43% | 3% | 57% |

| Beauty | 35% | < 1% | 65% |

| Home & Kitchen | 33% | 4% | 67% |

| Softlines | 28% | 9% | 72% |

| Books | 74% | < 1% | 26% |

| Consumables | 41% | 2% | 59% |

| Toys | 42% | < 1% | 58% |

Eighteen Amazon Marketplaces

Amazon launched in Sweden on October 28th, becoming its 18th global marketplace. Few Swedish businesses - less than a hundred - had joined the marketplace, but more than forty thousand worldwide sellers were present at the launch. Many products on Amazon Sweden came from auto-translated listings on other Amazon marketplaces, which enabled it to have a deep catalog on day one, but had unfortunately resulted in many wrong, sometimes comical, and even offensive Swedish translations.

Amazon launched in Saudi Arabia on June 17th, replacing Souq.com - the largest e-commerce platform in the Arab world it acquired for $580 million in 2017 - with Amazon.sa. Saudi Arabia was Amazon’s 17th global marketplace. It launched with close to 8,000 sellers.

Amazon launched in the Netherlands on March 10th, its 16th global marketplace. Over a thousand local retailers and more than thirty thousand worldwide sellers were present at the launch. Amazon has been selling e-books for Amazon Kindle in the Netherlands since 2014, as well as it provided access to three million items from Amazon.de since 2016.

Forty thousand sellers at Sweden’s launch were more than any previous Amazon’s new market. The previous record was its launch in The Netherlands with thirty thousand sellers. Nearly all of the sellers in Sweden and The Netherlands marketplaces were existing sellers from its other European marketplaces. When launching in new European countries, Amazon utilizes sellers it has attracted elsewhere to kickstart the initial supply. Thus, most sellers in the Sweden marketplace were from China, Germany, the U.K., Italy, Spain, and France, who joined with a single click of a checkbox.

In Europe, the hundreds of thousands of third-party sellers, the assortment they provide, and Amazon’s expanding fulfillment network that reaches most of the continent in two to three days are keys for future expansion. Combined with the auto-translated catalog and reviews, the cost to launch new countries for Amazon is ever-decreasing. That means Amazon will enter markets it has previously deemed too small.

Amazon.com remains the company’s most important market, representing nearly 46% of total visits across its worldwide marketplaces. The next three - Japan, Germany, and the U.K. - command 10%. Together with India, the top five markets represent nearly 80% of web traffic.

Three years ago, Amazon launched in Australia. Since December 2017, Amazon spent the first twelve months scaling the infrastructure and introducing FBA and Prime services, which opened to memberships in June 2018. Fueled by those, Amazon continued to grow, surpassing 40 million monthly visits in November 2020. It had just 25 million in November 2019 and 16 million in November 2018. Australia offers a glimpse of what Amazon could do in new markets.

When Amazon launches in new markets, it often attracts outsized attention and high expectations. Most shoppers get disappointed with prices, selection, and the service offering. Nonetheless, Amazon continues to grow and slowly catches up with those expectations. Australia is the best example of that.

Etsy

Etsy has used surging demand for face masks to accelerate growth for all handmade and vintage goods. After growing 20% for the last five years, it nearly doubled GMV in 2020. Thus, Etsy reached a GMV level it wouldn’t have gotten to for at least three years. Etsy’s success this year was synonymous with face masks. However, face masks represented only 20-25% of GMV growth. Instead, they were the most impactful by bringing more buyers to the marketplace that drove more sellers to join.

The company reported selling $346 million worth of face masks in the second quarter and $264 million in the third quarter. On April 3rd, the same day the White House announced guidelines that Americans should wear masks outside of the home, Etsy sent a push notification to every seller: “Calling all sellers. Start making face masks.” Hundreds of thousands of existing and new sellers started selling face masks.

“I woke up to discover it was suddenly like Cyber Monday,” Etsy’s CEO Josh Silverman told the Financial Times. “But everyone in the world wanted only one product.” That product was face masks.

Since Etsy made that call to sellers, the marketplace entered into a growth run it hasn’t seen for years. In April, “face mask” was the most frequently searched term on Etsy. But buyers didn’t only buy face masks. And because they bought other goods as well, sellers flooded in to offer them.

Etsy added 1.9 million new sellers in 2020, up from one million last year. There was a visible acceleration in April, and it has sustained so far - it was adding 200,000 new sellers monthly for the second half of the year, more than double the amount before the pandemic started.

New sellers increased the total catalog size - Etsy finished the year with over 80 million products, up from 60 million at the start of the year. The increase was across the board, with Home & Living, Art & Collectibles, and Jewelry departments leading.

Half of the new sellers were U.S.-based. That’s a considerably higher share than over the past few years. Etsy has international sellers and buyers and has, in the past, made growing internationally one of its key goals (35% of its sales are international). However, the pandemic brought nearly a million new U.S.-based sellers to Etsy.

Etsy’s number of active sellers increased by over a million in a year because many of the newly joined sellers and some older sellers who had forgotten Etsy had a sale.

Walmart

Walmart’s marketplace GMV more than doubled in 2020. In the third quarter, marketplace sales grew “triple-digits” (over 100%) while overall e-commerce sales were up 79%. The marketplace sales also grew at least 100% in the second quarter, according to the company. In the first quarter, the company said that while overall e-commerce business grew 74%, growth in the marketplace outpaced it.

“Growth was strong in pickup and delivery as well as direct-to-home with the highest growth coming from marketplace,” said Doug McMillon, CEO at Walmart, when discussing third-quarter results. John R. Furner, CEO at Walmart U.S., described the marketplace as “the overall winner in the eCommerce business” when asked by UBS Securities analyst Michael Lasser what contributed the most to the improving e-commerce margin.

On February 25th, Walmart announced Walmart Fulfillment Services (WFS) that allows third-party sellers to store and fulfill inventory from Walmart’s warehouse. However, the service is powering less than 0.1% of the two-day enabled products. Only 430 sellers have started using the service by the end of the year, and WFS powers only 15,000 products.

Walmart introduced the service with the “If You Build It (Together), They Will Come” headline. A callback to the 1989 film Field of Dreams about an Iowa corn farmer who hears a voice telling him: “If you build it, he will come.” He interprets this as an instruction to build a baseball diamond. Unfortunately, in business, the strategy rarely works.

Adopting a marketplace’s fulfillment service depends little on the rates offered but on whether it enables more sales revenue than the storage, fulfillment, and overhead costs. Few marketplaces have that balance tipped positively to the sellers. In the U.S., there is only one - Amazon’s Fulfillment by Amazon (FBA). For example, if a seller has a few products selling 100 units a month, then storing those in the marketplace fulfillment service is often a good strategy. Because doing so enables fast-shipping tags on that marketplace and thus further increases sales. On the other hand, if the seller has thousands of products, but each individually sells only a few units a month, the low sell-through rate renders the fulfillment service not worth the extra overhead.

Most of Walmart’s sellers do not have items with high enough sell-through rates. Walmart Fulfillment Services thus solves a problem very few sellers have. The marketplace is not big enough to demand marketplace-specific fulfillment service.

On June 15th, Walmart announced a partnership with Shopify. The mutual partnership announcement set a goal to add 1,200 Shopify stores to the Walmart marketplace by the end of the year. This goal was quickly surpassed by the end of June instead. But, it is not a key metric. Instead, it is the number of successful stores that matters, and that will take time to crystalize. Despite Walmart attracting hundreds of millions of visits every month, products on the website do not get discovered purely by being on it.

Walmart marketplace has nearly 70,000 sellers, doubling in size from 2019. The partnership with Shopify has accelerated its growth. Despite the continued increase in the number of sellers, the total catalog size has decreased by five million. The decrease occurred from a few large marketplace sellers delisting their catalogs, mainly in the Books and Home departments. The marketplace still represents 90% of the overall assortment, despite the shrunken catalog.

Target

Nearly two years since launch, Target’s invite-only marketplace has grown to 255 merchants and 165,000 products. This group of US-based retailers and brands have expanded Target’s assortment, and some of them reported impressive growth figures; however, overall, the marketplace remains a tiny experiment for Target.

On February 25th, 2019, the company launched a marketplace called Target+, or Target Plus. It started with 30 merchants and 60,000 products. The most significant difference is that Target’s marketplace is invite-only, meaning merchants and brands on it are selected by the company instead of more open marketplaces of other retailers.

“Stores enabled more than three-quarters of Target’s digital sales,” said Brian Cornell, CEO at Target, discussing second-quarter results. The company added that “More than 90% of our Q2 sales growth involved our stores, whether a guest’s order was purchased at the register, put in their car or shipped from a store.”

The marketplace is a standard tactic to expand the selection, but it doesn’t fit with a lot of other strategic moves that made Target successful online. Stores enable same-day fulfillment options, such as in-store pickup, drive-up, and delivery with Shipt. The problem, which was as accurate when it launched as it is today, is that the marketplace doesn’t leverage Target’s strengths. Those same strengths that enabled most of the digital sales growth since Target+ launched.

The one area where the Target+ remains compelling is its ability to be a stepping stone for brands to join Target online and offline - despite being invite-only, it takes significantly less effort to start selling that becoming a Target vendor. It could act as a risk-free testing ground for the company to onboard smaller brands and test their products’ demand.

eBay

eBay’s GMV grew 26% in the second quarter and 22% in the third quarter, a remarkable acceleration from the 2% average over the past thirteen quarters. After declining sales in every quarter of 2019 and the first quarter of 2020, the pandemic drove a wave of shoppers to rediscover eBay. eBay benefited from reduced online advertising competition and Amazon’s focus on essentials too. The number of products available and the number of businesses selling on eBay didn’t increase significantly. However, more buyers have resulted in increased overall marketplace liquidity.

Despite sales growth for the first time after years of stagnation, eBay still underperformed the market - U.S. e-commerce growth was faster than eBay’s performance. Perhaps the best visualization of this is that Shopify processed more transaction volume in the second quarter than eBay. Shopify is not a marketplace directly comparable to eBay; however, like all e-commerce companies, they compete for the same customers. Shopify is merely an example of how much progress is possible with the right e-commerce solution for the right time - five years ago, Shopify was ten times smaller than eBay.

eBay sold its classified ads business for $9.2 billion in July 2020 after agreeing to sell StubHub for $4.05 billion in late 2019. Activist investors pushed the company to slim down its operations. However, it made little progress in anything else. eBay is both a success, surpassing $90 billion in merchandise sold this year, and is mostly excluded from the conversation about retail’s future. It benefited from the surge in online shopping in 2020, but it is unlikely to retain that momentum.

Wish

Launched in 2011, Wish is a mobile shopping app for customers whose priority is low prices. While relatively unknown to non-users, the app is one of the most downloaded shopping applications for both iPhone and Android phones, consistently in the top 5 for both platforms. It is the latest e-commerce company to go public in December 2020.

“Today, most of our merchants are based in China,” wrote Wish in its Form S-1. “We initially grew our platform focusing on merchants in China, the world’s largest exporter of goods for the last decade, due to these merchants’ strength in selling quality products at competitive prices.” However, the company has been trying to recruit merchants outside of China more aggressively this year, “The number of merchants on our platform in North America, Europe, and Latin America has grown approximately 234% since 2019. In particular, the number of merchants on our platform in the U.S. has grown approximately 268% since 2019.”

Only 45% of sellers added in 2020 were China-based. More merchants came from the U.S. instead. In the past, China-based sellers would make up more than 90% of the total. However, as is always the case with marketplaces, few merchants ever become active or grow to represent a meaningful share of the total sales. Over 90% of active sellers on Wish are still from China.

2020 was a tremulous year for Wish because it relies on China-based sellers. Its core marketplace revenue (the revenue it collects from charging a commission on each transaction) grew the most in the second quarter. However, the first quarter had negative growth, and the third quarter was much slower than the second. Core marketplace revenue growth follows GMV growth.

The company explained the first-quarter decline as “In January and February of 2020, businesses across China were impacted by the initial outbreak of COVID-19 before the virus spread globally, and many businesses shut down due to nation-wide lockdowns.” By the second quarter, sellers in China reopened, and Wish also benefited from increased overall demand.

However, it “experienced severe disruptions in the global logistics network that affected delivery times to our buyers around the world,” which impacted buyer engagement and retention in the third quarter. In the United States, the average “time-to-door” was 62 days in the second quarter of 2020. It recovered to 22 days in the third quarter. Its growth in the third quarter was considerably slower than the second because many shoppers had to wait for months to get the orders they placed in the previous quarter.

Wish has launched efforts like Wish Local and continues to invest in its delivery network Fulfillment by Wish (FBW). But it is facing risks beyond fulfillment speed, and it is unclear if the playbook that got it to this point will continue to scale.

Google Shopping

In July, Google announced that it would take steps to bring more sellers and products onto its shopping marketplace by reducing commission fees to zero. However, there was no noticeable acceleration in the number of sellers. The marketplace did double in the number of sellers from 2019 but has remained at a consistent growth rate.

Bill Ready, President of Commerce Google, wrote in the announcement, “By removing our commission fees, we’re lowering the cost of doing business and making it even easier for retailers of all sizes to sell directly on Google.” These changes make Buy on Google the only marketplace in the U.S. with zero fees. Fees on other marketplaces range from five to fifteen percent.

Buy on Google is a marketplace inside of Google Shopping that allows customers to check-out without leaving Google. Customers discover products by going directly to the Shopping tab, using the Google Shopping app, or seeing Google Search ads. However, few customers are aware of Google Shopping, let alone of Buy on Google, and thus liquidity on the marketplace is minimal. Few sellers have used it themselves as customers too. Therefore, zero percent fees instead of fifteen percent on tiny sales is an insignificant change.

“We want to make sure selling online is easy and inexpensive,” said Bill Ready in an interview with the New York Times. These are not challenges for most sellers. Instead, the challenge is customer acquisition. Google has no solution for that outside of the advertising business it had for decades. The company continues to build supply by adding more sellers but has little to show for creating demand.

2021

Going into 2021, fundamentals like software, agencies, fulfillment, advertising, and financing are key. They power the flywheels of e-commerce and will continue to attract capital. Enabled by them, Amazon, as well as the other marketplaces, will get bigger.

But this whole space can be thought of more broadly.

“In a world of abundance, being able to aggregate demand is more valuable than being able to create supply,” wrote Ben Thompson of Stratechery. Paraphrased for e-commerce, the most valuable asset is shoppers, not the supply of products. In that light, the efforts marketplaces spend on attracting sellers and growing the assortment is table stakes. A much more important effort - perhaps the only important effort - is fostering demand. Marketplaces do not compete for sellers - they compete for shoppers.

Nowhere is this more apparent when comparing Google Shopping to Amazon. Google Shopping is working on matching Amazon’s supply of products (a Sisyphean task by itself), while Amazon is enriching the Prime membership. Supply will come as long as Prime members come to shop on Amazon. But shoppers won’t abandon Amazon just because Google now has the same products. Although many shoppers buy goods on Walmart, they could get on Amazon for the same price from the same seller and vice versa (marketplaces are converging in having identical assortment).

The importance of demand goes further. E-commerce is breaching into non-retail avenues - like social networks - because it follows audiences. For some shoppers, buying a brand from a retailer versus buying it from an influencer’s account on Instagram is the same. Thus, the efforts of Facebook and Instagram in shopping are notable. Those apps already have more demand than most retailers, and ads on them have been powering e-commerce for years. It doesn’t take much to transition into a fully-fledged shopping destination. Facebook made more progress this year than practically the rest of the industry combined.

Shopping on Instagram doesn’t look anything like shopping on Amazon, but powering them is the same marketplace model. There are also - and will be even more - niche marketplaces that focus on a vertical or an audience. They naturally attract demand. But they also look less than Amazon and more like something different. The demand comes not because “we are not Amazon.” It took most retailers decades to figure out how to differentiate online, but in 2020, those that had buy-online-pick-up-in-store flourished. Demand follows differentiation.