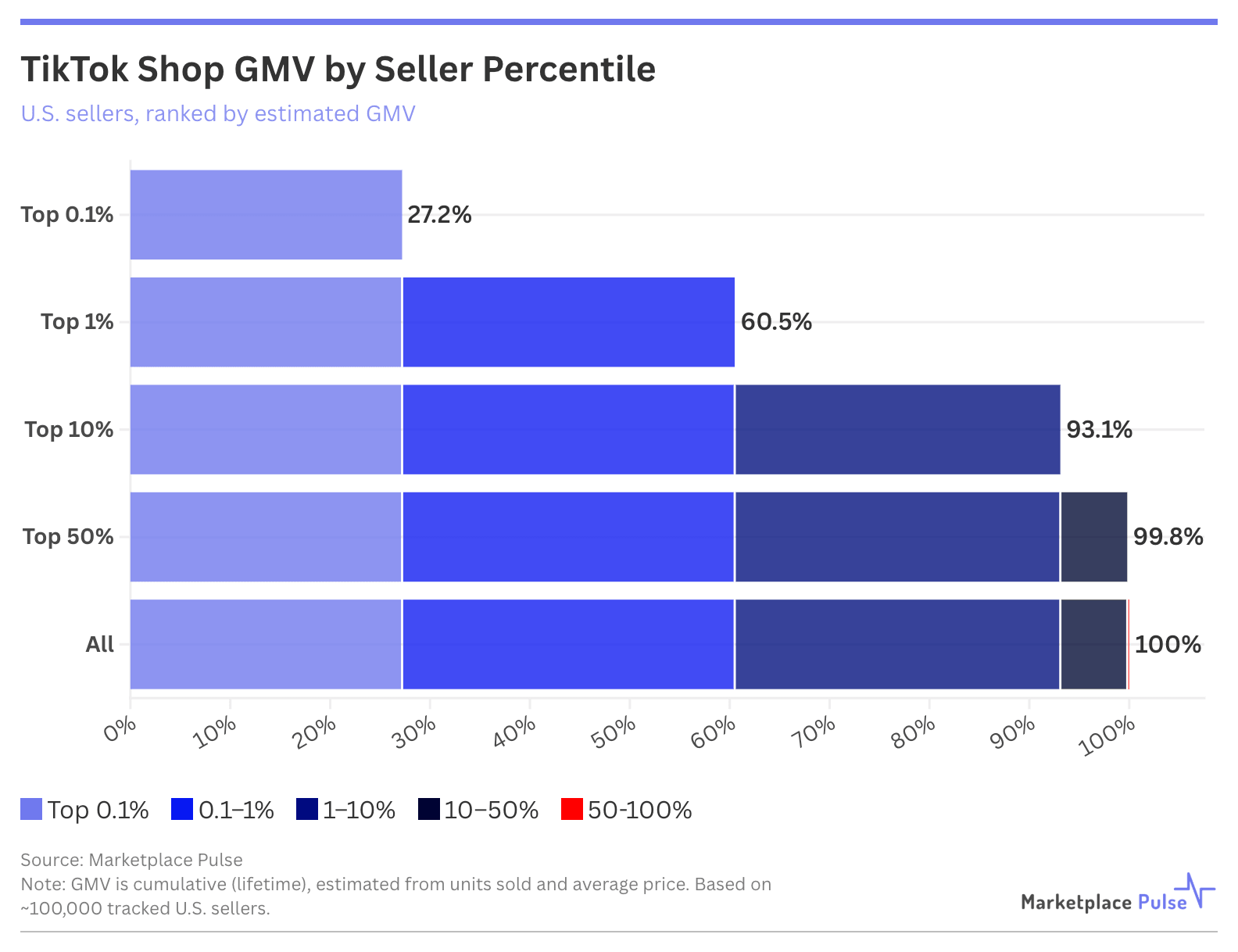

TikTok Shop was built on the promise that anyone can win. Discovery runs on content rather than search; the algorithm decides what surfaces, and one video can take an unknown seller to the top of a category overnight. Yet early Marketplace Pulse data on nearly 100,000 U.S. TikTok Shop sellers points the other way: the platform has produced a seller economy more top-heavy than the search-and-advertising marketplaces it set out to disrupt. The top 1% of sellers drive 60% of all U.S. GMV tracked, and the top 0.1% – fewer than 90 sellers, each averaging over $100 million in lifetime sales – account for more than a quarter of it.

That concentration runs deeper than on Amazon, where fewer than 8,000 sellers, about 1.6% of the active base, generate half of its third-party GMV. On TikTok Shop, the top 1% of tracked sellers clear that same 50% threshold with room to spare. That 1% – fewer than 900 sellers – are overwhelmingly multimillion-dollar operations, while the bottom half of sellers in the data contribute roughly 0.1% of GMV. The middle is thin. The platform that removed the paywall on discovery has not flattened outcomes. It has sharpened them.

The data is early. Marketplace Pulse now tracks close to 100,000 U.S. TikTok Shop sellers, capturing the platform’s largest sellers comprehensively, with the long tail still filling in. GMV here is lifetime, estimated from units sold and average price rather than a period figure, so the concentration is best read as a distribution of who has captured demand to date, not a measure of current run-rate. As coverage reaches further into the tail and time-period data comes online, the long-tail percentages will move, and monthly GMV will sharpen the picture. The shape, however, is unlikely to change.

Platform curation reinforces the pattern. TikTok Shop assigns sellers badges, with Official Store and Gold Star tiers marking the verified, higher-performing merchants it surfaces most prominently. Official Store sellers move roughly 40 times the volume of unbadged sellers, at a higher average price; Gold Star sellers move close to 18 times the volume. Badging is partly a consequence of scale rather than a cause of it, but the effect compounds. The platform’s own signals point demand toward sellers who have already broken through.

This complicates the content-first thesis that has defined TikTok Shop since launch. The pitch was that owned attention could replace paid placement, letting creators and small brands skip the advertising arms race that defines Amazon. For the few who go viral, it does. But it lands on the same dynamic now shaping the maturing marketplace economy: as platforms mature, the bar for execution rises and revenue concentrates among the few who clear it. On Amazon, the filter is operational sophistication and capital. On TikTok Shop, it is virality, which turns out to be its own kind of scarcity. Democratized discovery, so far, has produced a smaller winners’ circle, not a wider one.