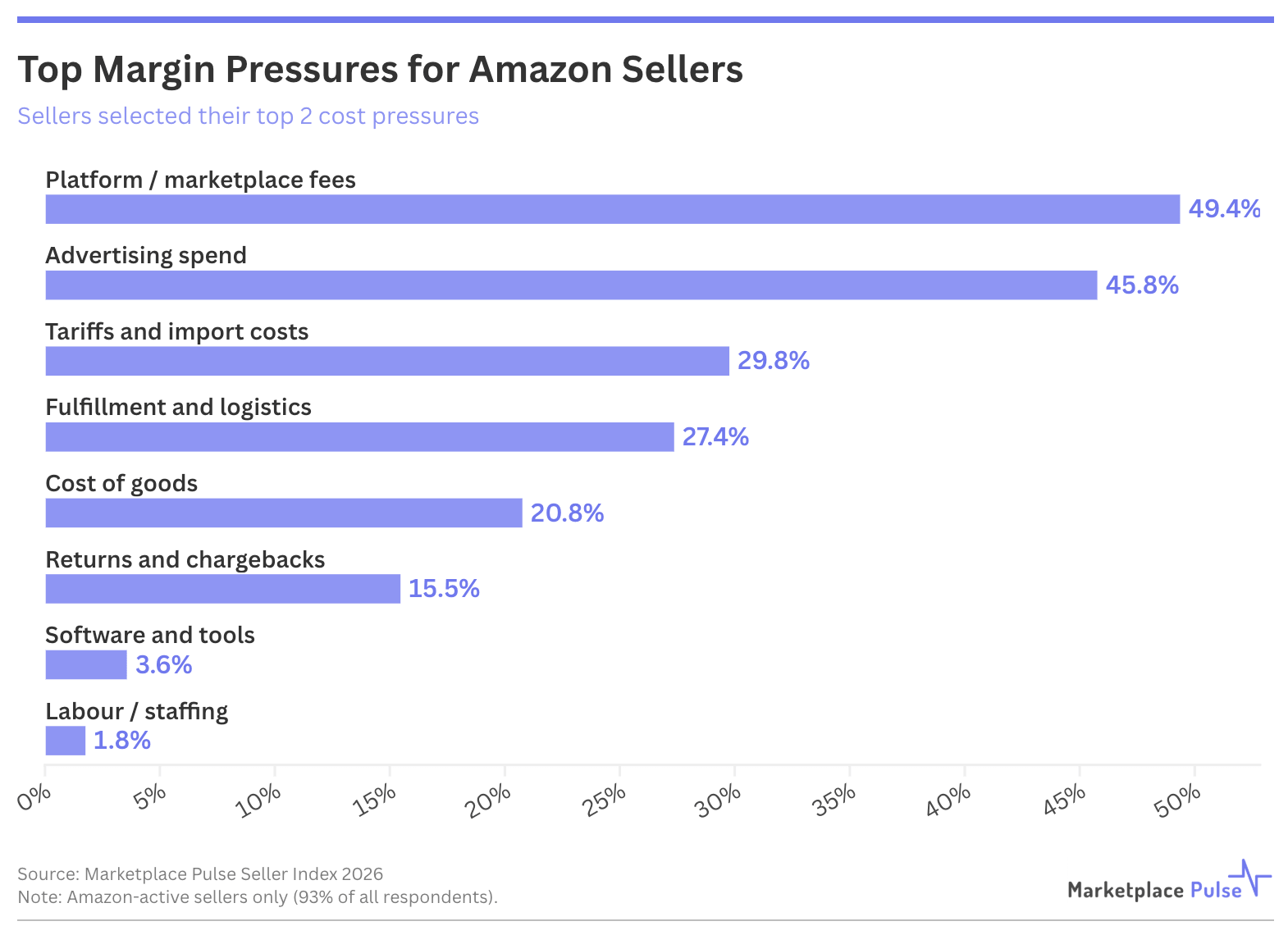

Half of Amazon sellers cite platform fees as a top-2 cost pressure, yet less than a quarter are actively reducing their Amazon dependence. According to Marketplace Pulse’s 2026 Seller Index, 49% of sellers active on Amazon identified marketplace fees as their primary margin concern, nearly matched by the 46% citing advertising spend. Together, these two platform-controlled costs represent the overwhelming pressure across the seller base. Yet among sellers most frustrated with fees, only 24% are reducing Amazon’s share of their revenue mix, while 42% are actively growing it.

Amazon controls 36% of U.S. e-commerce and 70% of marketplace commerce, making it the unavoidable market opportunity. Sellers remain built for and around selling on Amazon, unable to diversify to other channels that collectively represent the remaining 30% of marketplace commerce. The survey captured sentiment before three rapid policy changes stress-tested that dependence: a 3.5% fuel surcharge, automatic ad cost deduction from proceeds eliminating credit card cash-back opportunities, and DD+7 disbursement terms pushing payment seven days post-delivery. Together they removed a financial float sellers with declining margins depend on – 47% reported year-over-year margin decline.

Some sellers organized an advertising boycott for April 15. Amazon rolled back the ads payment change the day before, delaying until August. Even assuming 1,000 high-volume sellers ($10 million annual revenue, 10% ad spend) boycotted for the full day, the impact would total roughly $3 million – less than 2% of a typical day’s revenue from an ad business generating nearly $70 billion annually. The rollback was less about lost dollars and more about regulatory optics during the ongoing FTC antitrust case and about managing seller sentiment, given that its active seller pipeline has contracted.

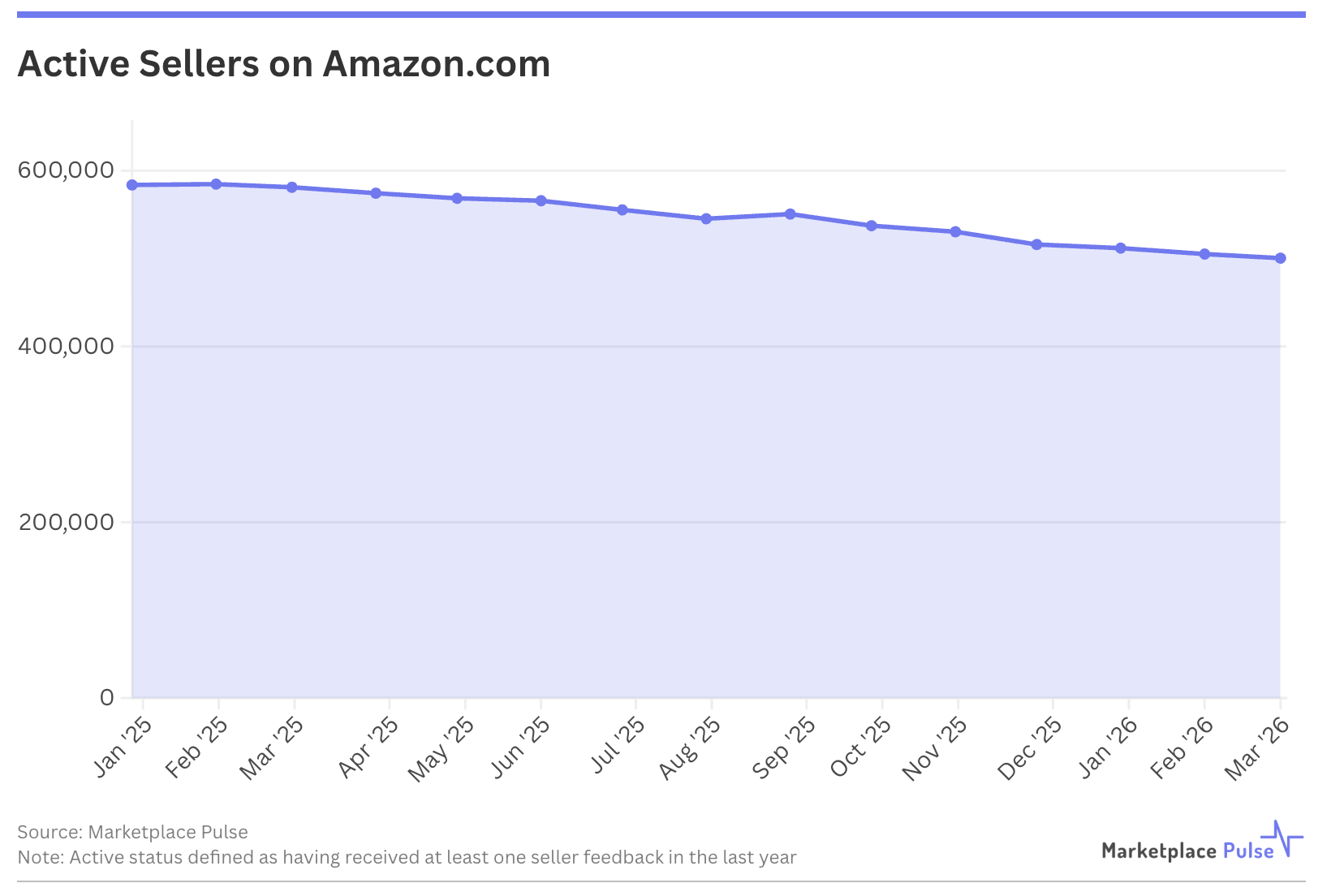

According to Marketplace Pulse data, active seller count on Amazon.com has declined from 584,000 in January 2025 to 500,000 in March 2026, following a decade of seemingly unlimited supply growth. Rising fees, intensifying competition, and compressed margins have raised the execution threshold – fewer sellers can sustain profitable operations. Meanwhile, revenue concentration has intensified: fewer than 8,000 sellers now generate half of Amazon’s estimated $300 billion in U.S. third-party GMV, down from 15,000 sellers holding that position less than three years ago.

Amazon is applying its own “your margin is my opportunity” principle to sellers – third-party seller fees and advertising now generate roughly a third of total company revenue. Yet it simultaneously becomes more reliant on a seller base that accounts for 62% of units sold and, according to Marketplace Pulse GMV estimates, roughly 69% of total GMV. The relationship has shifted from effectively unlimited supply to high-stakes mutual dependence.

Sellers are frustrated with platform fees yet deepen their dependence on Amazon because alternatives don’t offer comparable scale. Amazon extracts more revenue from sellers while becoming more vulnerable to a concentrated base that could, in theory at least, coordinate or exit. Both sides are locked in – sellers by Amazon’s market dominance, Amazon by its dependence on a contracting and concentrating seller base that drives the majority of store activity. Continued fee increases and seller exits tighten this mutual dependence while making it more precarious.